Should I trade New Fortress Energy or NFE? A Risk-Impact and Scenario-Based Analysis

New Fortress Energy (NFE) is a fast-moving LNG infrastructure and services company that has taken aggressive growth and financing steps since 2021. By 2025 the company faces a high-stakes mix: heavy leverage and recent quarterly losses on one hand, and newly inked long-term contracts and asset sales on the other. The near-term investor question is whether the operational wins (long-term contracts, portfolio simplification) are sufficient to stabilize cash flows and restructure debt — or whether deeper balance-sheet remedies will be needed. Reuters+2businesswire.com+2

1) Quick factual baseline (what matters for the analysis)

-

Financial performance: In early-to-mid 2025 NFE reported sizable quarterly losses and weak margins across segments; management highlighted restructuring and asset sales as remedies. Reuters

-

Balance sheet and liquidity: The company entered 2025 with high long-term debt (reported around several billion USD) and actively pursued asset sales and liability restructurings to shore up liquidity. The sale of Jamaican assets (completed in mid-2025) was a material deleveraging step. businesswire.com

-

Regulatory / compliance items: NFE received a Nasdaq notice for delayed SEC filings in 2025, triggering a 60-day compliance window — a governance/market-access risk until resolved. Reuters

-

Commercial wins: In September 2025 NFE announced a multi-year LNG supply agreement with Puerto Rico (reported as materially large, multi-billion over the contract life), which, if approved and executed, strengthens contracted volume visibility. Reuters

-

Restructuring rumors: As of late October 2025 the company was reported to be exploring a UK restructuring process (scheme of arrangement) as an alternative to a U.S. Chapter 11 — a sign that management is weighing formal debt workouts to preserve contract value. Bloomberg

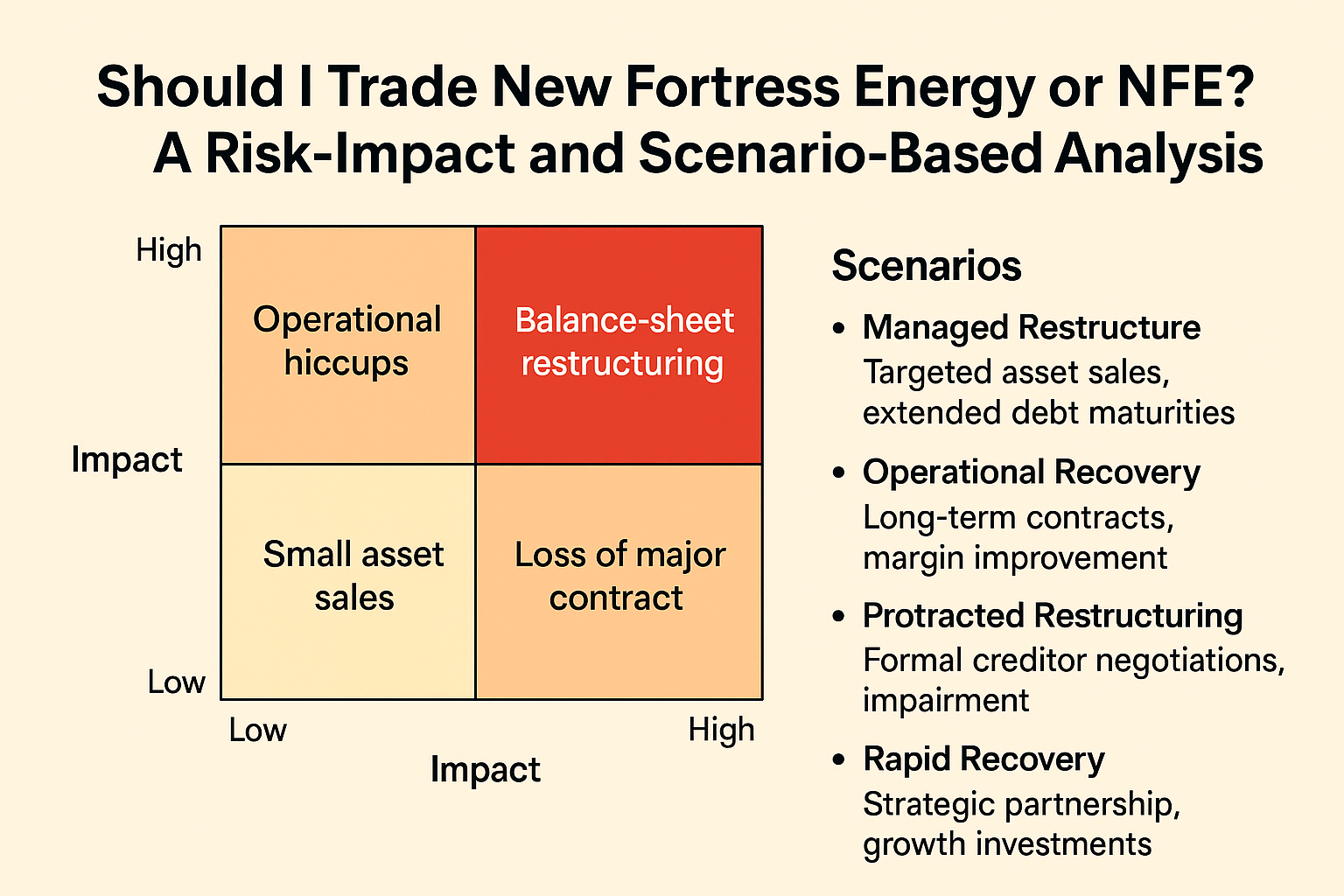

2) Risk-Impact matrix — prioritized view (textual)

| Likelihood / Impact | Low Impact | High Impact |

|---|---|---|

| High Likelihood | Operational hiccups - Possible LNG shipping or terminal downtime. - Causes short-term EBITDA erosion but manageable. Short-term EPS volatility - Linked to delayed SEC filings or restructuring headlines. |

Balance-sheet restructuring or UK scheme of arrangement 🔴 - Highly probable due to leverage and liquidity pressure. - Major financial consequences for equity and creditors. Difficulty securing long-term counterparties - High likelihood because of sub-investment-grade rating and high financing costs. |

| Low Likelihood | Small asset sales / minor divestments - Manageable events with limited strategic effect. - May slightly improve liquidity but not change debt metrics significantly. |

Loss of major contract or litigation risk ⚠️ - Low probability but extremely damaging if occurred. - Could erase key revenue streams and impair asset valuations. Fire-sale asset disposals - Rare but could permanently damage future earning potential. |

3) Scenario-Based Analysis (2025–2027) — four scenarios

| Scenario | Assumptions | Expected Outcome | Probability | Financial Impact / Implications |

|---|---|---|---|---|

| Scenario 1 — Managed Restructure (Base Case) | - Jamaica asset sale completed.- UK scheme or negotiated debt extension successfully implemented.- Puerto Rico contract approved and executed.- No major new liquidity shocks. | - Liquidity stabilized through extended maturities.- EBITDA recovers gradually.- Creditors cooperate under restructuring plan.- Shareholders retain partial value. | Medium–High | - Improves free cash flow stability.- Moderate stock recovery likely.- Sets foundation for future refinancing and growth. |

| Scenario 2 — Operational Recovery + Market Re-Rating (Bullish) | - Multiple long-term LNG supply contracts signed.- Successful refinancing with reduced interest burden.- LNG demand and pricing environment favorable.- Investor sentiment improves. | - Revenue growth 10–20%.- Strengthened balance sheet and margin improvement.- Equity re-rated upward by market. | Medium | - Strong EBITDA and net income upside.- Potential stock price rebound 50%–100% from distressed levels if momentum sustained. |

| Scenario 3 — Protracted Restructuring / Value Impairment (Bearish) | - Asset sales insufficient to meet debt obligations.- Creditors demand deeper restructuring terms.- Some contracts delayed or canceled.- Governance challenges persist. | - Extended legal and financial restructuring process.- Shareholder dilution or impairment likely.- Slow operational turnaround. | Medium–High | - Equity value erosion.- Risk of further rating downgrades.- Institutional investors exit positions. |

| Scenario 4 — Rapid Recovery + Strategic Consolidation (Optimistic) | - Strategic partner or private equity infusion.- Strong execution of LNG contracts (Puerto Rico and others).- Efficient deleveraging with debt-to-equity swap or new funding.- Improved sentiment in LNG markets. | - Quick liquidity restoration.- Resume new LNG terminal investments.- Enhanced credibility with investors and creditors. | Low | - Major equity revaluation (possible 2–3× upside).- Strengthened long-term sustainability.- Company exits distressed category entirely. |

4) What investors should watch (signals & timings)

-

Debt restructuring updates / UK scheme filings: This is the single most material governance event; it determines creditor priorities and possible equity outcomes. Bloomberg

-

Contract approvals (Puerto Rico and similar): Contract execution and payment terms materially affect revenue visibility. Reuters

-

Quarterly cash balance and unrestricted cash: Liquidity trumps everything in distress scenarios. Look for management guidance on covenants and maturities. Reuters

-

SEC filing / Nasdaq compliance: Timely 10-Q/10-K filings and audit stability will reduce market/legal uncertainty. Reuters

5) Investment takeaway and risk checklist

For traders (short term):

-

Expect volatility tied to restructuring headlines and quarterly prints. Trading is high-risk; position sizing and stop rules are essential.

For longer-term value seekers:

-

The equity story is contingent on credible deleveraging and contract execution. If you believe management can preserve contract economics and extend debt maturities, upside exists — but the path is risky and may include dilution.

Red flags to avoid

-

Failure to execute planned asset sales at expected prices. businesswire.com

-

Adverse creditor rulings that force accelerated maturities. Bloomberg

6) Conclusion

By late-2025 New Fortress Energy sits at an inflection point: tangible commercial wins (long-term contracts) and portfolio simplification are positive signs, but high debt, repeated quarterly losses, SEC filing issues, and active consideration of formal restructuring increase execution risk. Investors should monitor restructuring process milestones, counterparty approvals, and cash runway closely. In portfolio terms, NFE is a high-risk, event-driven trade where outcomes range from recovery (if contracts and deleveraging hold) to significant equity impairment (if creditors press for value extraction). Bloomberg+4Reuters+4businesswire.com+4

Sources (key load-bearing references)

-

Reuters — “New Fortress Energy posts quarterly loss…” (May 14, 2025). Reuters

-

New Fortress Energy / BusinessWire — Completion of sale of Jamaica assets; Q1 results (May 14, 2025). businesswire.com

-

Reuters — Nasdaq non-compliance notice reporting (May 27, 2025). Reuters

-

Reuters — Puerto Rico LNG contract announcement (Sept 16, 2025). Reuters

-

Bloomberg — Reports on UK restructuring option (Oct 28, 2025). Bloomberg