🔷 Should I trade AES Corporation or AES? A Risk-Impact and Scenario-Based Analysis

The AES Corporation (NYSE: AES) stands as one of the world’s leading diversified power generation and utility companies. Headquartered in Arlington, Virginia, AES operates in more than 14 countries with a portfolio exceeding 31 gigawatts (GW) of generation capacity.

As the global energy landscape transitions toward decarbonization, AES has repositioned itself from a conventional thermal power producer into a clean energy and storage solutions leader, emphasizing renewables, battery storage, and smart grid innovation.

However, as of 2025, the company’s path forward is not without substantial risks and opportunities — spanning energy market volatility, debt exposure, project execution, and regulatory challenges.

This article provides a Risk-Impact and Scenario-Based Analysis to help investors understand AES’s strategic positioning and potential outcomes over the next 2–3 years.

🧩 1. Company Overview: AES in 2025

| Aspect | Details (2025) |

|---|---|

| Founded | 1981 |

| Headquarters | Arlington, Virginia, USA |

| CEO | Andrés Gluski |

| Market Capitalization | ~$13 billion (as of early 2025) |

| Business Segments | Renewable Generation, Energy Storage, Utilities, and LNG Infrastructure |

| Key Markets | United States, Chile, Brazil, Dominican Republic, Vietnam, Panama |

| Energy Mix (approx.) | 60% Renewable / 40% Conventional (coal, gas) |

| Strategic Focus | Accelerated clean energy transition and digital energy management via Fluence (its energy storage JV) |

AES has evolved into a renewable-first company, with a target of exiting coal completely by 2025–2026. It’s also a key player in grid-scale battery energy storage through Fluence, a joint venture with Siemens that recently went public (NASDAQ: FLNC).

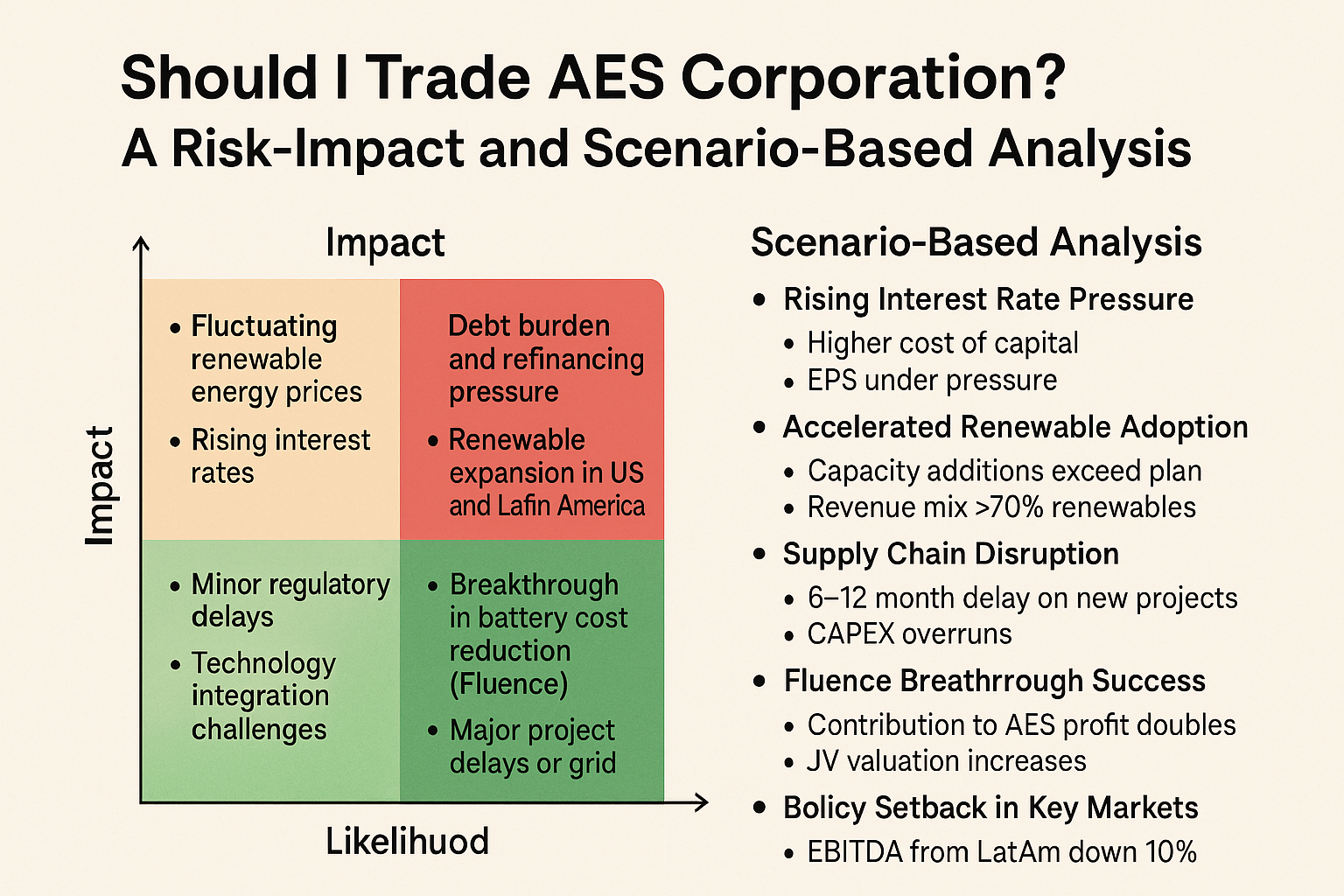

⚖️ 2. Risk-Impact Matrix (2025 Outlook)

Below is a Risk-Impact Overview for AES Corporation — balancing negative threats and positive opportunities across operational, financial, and strategic domains.

| Likelihood ↓ / Impact → | Low Impact | High Impact |

|---|---|---|

| High Likelihood | 🔸 Fluctuating renewable energy prices 🔸 Rising interest rates increasing cost of debt |

🔴 Debt burden and refinancing pressure 🟢 Renewable expansion in US and Latin America |

| Low Likelihood | 🔸 Minor regulatory delays 🔸 Technology integration challenges |

🔴 Major project delays or grid failures 🟢 Breakthrough in battery cost reduction (Fluence) |

Legend:

🔴 = Negative Risk | 🟢 = Positive Opportunity | 🔸 = Manageable Factor

✳️ Interpretation

-

High-likelihood / high-impact quadrant shows AES’s most critical challenge — its high leverage (debt over $20 billion) in a rising rate environment.

-

On the positive side, AES’s aggressive renewable growth across North and South America presents a high-likelihood, high-impact upside.

-

Low-likelihood / high-impact opportunities (like breakthroughs in storage technology) could dramatically reshape margins if realized.

⚙️ 3. Key Risk Categories Explained

🔻 A. Financial and Debt Risk

AES’s total long-term debt stands at around $20–22 billion, a legacy from its global expansion during the 2010s.

While much of it is project-financed and matched to long-term PPAs (Power Purchase Agreements), rising interest rates and refinancing costs in 2025 create significant stress.

Potential Impact:

-

Reduced free cash flow and dividend flexibility.

-

Lower credit rating outlook if leverage remains above 6x EBITDA.

Mitigation:

AES has begun rotating assets — selling legacy coal and natural gas plants to recycle capital into renewable and storage projects with higher margins and lower financing risk.

🔻 B. Execution and Supply Chain Risk

AES’s renewable pipeline exceeds 12 GW under development, primarily solar, wind, and battery storage.

However, project delays due to:

-

Permitting bottlenecks

-

Grid interconnection queues

-

Supply chain disruptions (e.g., battery cells, solar modules)

can postpone cash flow realization.

Impact: Medium to High

Likelihood: Medium

AES mitigates this via strategic partnerships (Siemens, Fluence) and long-term supplier agreements to secure components at fixed prices.

🔻 C. Regulatory and Policy Risk

Operating across 14 countries exposes AES to policy and foreign exchange volatility.

While the U.S. Inflation Reduction Act (IRA) boosts renewable incentives, emerging markets like Brazil and Chile carry policy uncertainty.

Impact: Medium to High

Likelihood: Medium

AES’s exposure to diverse jurisdictions reduces concentration risk but complicates compliance and reporting.

🔻 D. Climate and ESG Risk

Ironically, even as AES transitions to clean energy, it remains vulnerable to:

-

Extreme weather disrupting operations.

-

Public scrutiny of its remaining fossil assets.

-

ESG downgrades if coal phase-out lags schedule.

However, its ESG rating trend is positive, as S&P and Sustainalytics upgraded AES’s transition score in 2024.

🔻 E. Technological Opportunity

Through Fluence, AES benefits from AI-driven energy optimization, battery management software, and energy trading analytics.

If battery costs continue to fall below $100/kWh by 2026, AES could expand margins significantly.

Impact: High (positive)

Likelihood: Medium

🧭 4. Scenario-Based Analysis (2025–2028)

| Scenario | Key Assumptions | Expected Outcome | Financial Impact (approx.) | Strategic Implications |

|---|---|---|---|---|

| Scenario A: Rising Interest Rate Pressure (Negative) | - US 10-year yield stays above 4.5% through 2026 - AES refinancing costs increase by 200bps |

- Higher cost of capital - EPS under pressure - Dividend payout stagnates |

⚠️ EPS decline 5–7% annually | Accelerate asset recycling; refinance via green bonds; focus on low-debt geographies. |

| Scenario B: Accelerated Renewable Adoption (Positive) | - US and LatAm governments increase subsidies - Battery and solar costs fall 15–20% |

- Capacity additions exceed plan - Revenue mix >70% renewables |

🟢 EPS growth 10–15% | Become top-5 global renewable IPP; improve ESG score; attract green fund inflows. |

| Scenario C: Supply Chain Disruption (Negative) | - Global solar module shortage - Battery raw material inflation (lithium, nickel) |

- 6–12 month delay on new projects - CAPEX overruns |

⚠️ EPS down 4–6% | Hedge with diversified suppliers; localize sourcing; delay non-core projects. |

| Scenario D: Fluence Breakthrough Success (Positive) | - Fluence battery management AI achieves commercial scale - Software margins expand |

- Contribution to AES profit doubles - JV valuation increases |

🟢 EPS +8–12% | Reinforce position as energy storage leader; spin-off or expand AI platform. |

| Scenario E: Policy Setback in Key Markets (Negative) | - Brazil/Chile change renewable feed-in tariffs - FX volatility rises |

- EBITDA from LatAm down 10% | ⚠️ EPS -3–4% | Rebalance portfolio to US and Vietnam; hedge currency risk. |

📊 5. Summary: Likelihood vs. Impact Comparison

| Scenario | Likelihood | Impact | Net Effect |

|---|---|---|---|

| A. Interest Rate Pressure | High | High | Negative (Short-term) |

| B. Accelerated Renewable Adoption | Medium-High | High | Positive |

| C. Supply Chain Disruption | Medium | Medium-High | Negative |

| D. Fluence Breakthrough | Medium | High | Positive |

| E. Policy Setback | Medium-Low | Medium | Negative |

🔮 6. Strategic Outlook (2025–2028)

AES’s transformation story remains compelling but complex.

-

The company is no longer a “high-yield utility” — it’s becoming a hybrid clean-energy innovator.

-

Debt reduction and execution reliability are the top priorities.

-

The long-term thesis depends on sustained renewable deployment, AI energy management, and battery technology economics.

If management successfully navigates financing and regulatory hurdles, AES could emerge as one of the most profitable integrated renewable platforms in the Western Hemisphere by 2028.

🧠 7. Investor Takeaways

| Strengths (Opportunities) | Weaknesses (Risks) |

|---|---|

| Strong renewable growth pipeline | High leverage and refinancing exposure |

| Strategic JV in Fluence (energy storage AI) | Execution risk in global projects |

| Government support for clean energy (IRA) | Dependence on policy incentives |

| Diversified geographic footprint | FX and regulatory volatility |

| Improving ESG credentials | Vulnerable to rate-sensitive investors |

💬 8. Conclusion

In 2025, AES Corporation stands at a critical inflection point:

Balancing its ambitious clean energy transition against the realities of a capital-intensive industry and rising interest costs.

The risk-impact profile reveals that while financial leverage and execution risk are top threats, AES’s long-term opportunities in renewables, storage, and digital energy platforms remain highly attractive.

In a base-case scenario, AES delivers modest EPS growth (~5–7% CAGR) while de-risking its portfolio.

In a bullish scenario, driven by Fluence success and falling battery costs, AES could outperform peers in both growth and valuation re-rating.

For investors, AES offers a high-risk, high-reward play — best suited for those seeking exposure to the global energy transition with patience for volatility.